How’s business? Seems like an easy question to answer—we’re better, worse or about the same as last year. The reality is a bit more complicated. We talk about sales, but in fact, we should be talking about how much is left over at the end of the day—your bottom line.

Great management and great managers improve their profitability using many tools. One of these tools is a “costing model” that will be defined and discussed in this article. Here we will answer a better question: What drives net profit in your practice?

Net profit is what is left over at the end of any period of time after all revenue and expenses are booked accurately. Without sales there are no profits and most veterinary services (sales) have expenses that are directly and indirectly tied to performing that service. For example, a lameness exam at the farm cannot be done without several elements that have costs associated with the service: the veterinarian, a vehicle, tools to perform the exam, insurance, an office staff to book appointments and collect accounts receivable, rent or facility costs, and maybe medications to administer or dispense to treat the patient, etc. When we account for all of the costs involved in generating the revenue, the amount that is left over is the net profit for that specific procedure. When you combine the profitability of all the individual veterinary service procedures and subtract the costs associated with these procedures, the amount left over is the net profit in the business.

Which procedures make money, how much money, and why are they profitable? Are there procedures that are not profitable or are actually costing you money? Do you know what procedures are not profitable but considered valuable for your practice—called loss leaders? Do you understand the margins associated with the services you provide and the medications you sell?

Alphabet Soup

Activity Based Costing (ABC) (Figure A) is an analysis tool to help you understand profitability and the true costs associated with the revenue for a service. This business concept will help you better understand your business dynamics and develop the strategies necessary for both short-term and long-term profitable growth. This understanding will help you to make sound decisions in the future on where to invest time and money in your company.

ABC starts with a thorough review of what resources go into and come out of a specific procedure. The four key components necessary for the process are Data Collection, Allocation of Costs, Analysis and Action.

Data Collection

Revenue–This information is easily accessible in most practice management software programs. You provide a service and an invoice is generated for payment on that specific service. Expenses–Collection of this information is more challenging. Most management software programs account for the cost of inventory, but not the other operating costs of doing business. A wide range of resources is necessary to allow the veterinarian to deliver services to the patient. These include fixed overhead costs, labor costs, administrative costs, and inventory costs, etc. The size of the list depends on the size and complexity of your practice. It is a valuable exercise to think about ALL of the costs, obvious and hidden, that are required to allow you to perform a particular service.

Allocation of Costs

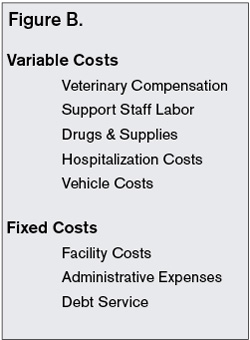

The cost allocation process assigns all possible costs necessary to perform a procedure. This is perhaps the most difficult and challenging part of the process, but it doesn’t have to be complicated to provide valuable information. Start by evaluating one or two current procedures. Costs are defined in two categories: variable costs and fixed costs.

Figure B illustrates a few of the costs in equine practice. Variable costs are the costs that change in proportion to the changes in the related level of activity or volume of the service offered and products sold. Fixed costs are costs that remain unchanged for a given period of time despite changes in activity or volume in the veterinary services performed. Your local accountant or industry consultant can help you start this allocation process. Each practice is unique and the information gathered must make sense for the practice setup and operations.

Analysis

Review the results and ask yourself, “Does this make sense?” Are there any major expenses that were left out? Does this procedure make money? What are the variables and tools I have at my disposal to improve the profitability of this procedure? Listed below are a few options to consider when analyzing your ABC procedure results to increase your profit margin.

· Decrease labor costs (doctor, service provider and/or support staff)

· Increase pricing

· Improve operational efficiency

· Increase volume and marketing

· Eliminate the procedure/service

· Add additional services or product sales to a procedure

It’s important that all analysis lead to some type of management activity, from small to dramatic changes. ABC provides a level of detail and a tool to analyze the activity of your business from a financial and operational perspective.

Action

Taking action is not easy. It needs to be communicated to all members of your team. Judgments are often made about management decisions without all of the facts at hand. Take the time to engage, empower and educate your staff about procedural and service changes that affect them and your patients. Incorporate team building and allow staff members to come up with their own suggestions about how to improve the bottom line. Clarity with employees in this process is paramount and helps a business move forward, maintaining and improving the bottom line.

Case Report

Green Pastures Equine Clinic (GPEC) is a progressive five-veterinarian equine hospital and ambulatory practice serving a broad group of horses from sport horses to backyard pleasure horses. Nestled in a competitive equine community, it enjoys both a large equine population and a fairly stable economy even during the recent nationwide financial challenges.

Recently, hospital profits have declined without a decline in patient visits to the facility.

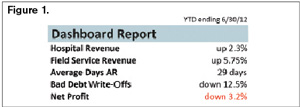

The owner, Dr. Jones, has been working hard and is busy as usual, but as the busy season slows, she notes that the practice is not on target to hit her business goals and at the end of the third quarter she doubts there will be enough profits to take any owner dividend or give bonuses to her associates as she was able to do last year. A simple dashboard management report paints a picture of the first six months of 2012 and a snapshot of the financial health of the business (Figure 1).

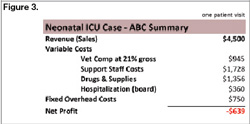

Dr. Jones has a feeling that some of her ICU cases are not very profitable even though the practice has had very successful patient outcomes and the case load is starting to increase for these types of procedures. She decides to conduct an ABC analysis of ICU cases by looking at neonatal foal care since she has all the data fresh from the busy foaling season (Figure 2).

One particular case illustrates common and repeatable findings for this type service provide by GPEC (Figure 3). In this medical case, a 36-hour Arabian “dummy” foal is admitted to the clinic. Extensive lab work, 24-hour intensive care, plasma, fluids and antibiotics are used over a six-day period and a successful outcome is obtained, with both mare and foal leaving the facility with happy owners.

Using the information provided, consider the following regarding the financial health of this practice and the ABC example of the intensive care patient.

· How can ABC analysis be used in this case?

· Why are the short-stay foal cases profitable and the longer-stay are cases not? What potential costs might account for these differences?

· What management options are available to improve the profitability of these cases?

· What other metrics (measurements) might be helpful in your analysis?

· What changes could be made, and if you made them, how would you implement those changes in your practice today?

· How would you know whether the changes you made are successful?

A detailed discussion addressing the questions from the sample case above may be found on the resource page of the website www.equinebusinessmanagementstrategies.com. In addition, other resources and report templates are included on this site and may be downloaded free of charge to help you begin this ABC analysis for your practice.

Summary

Activity Based Costing (ABC) is a great management tool to help understand where money is made and how to improve the operating efficiencies of a business. The case of Green Pastures Equine Clinic is an example of the increasing cost of doing business in equine practice today. Without detailed examination of many of the common procedures performed and an assessment of new options for services it is easy to see how gross revenue can increase and net profit decrease.

Each one of the metrics outlined in the charts is a piece of the puzzle that provides insight into the health of the practice. Most importantly, these metrics provide clues to help develop changes and promote growth and prosperity for the practice. Start slow, and dig into the details of how your practice generates true net profit by analyzing the activities of daily operations–sales and costs. ABC is not as easy as learning the alphabet, but Activity Based Costing is worth the extra effort and energy to learn where and how you make money in your business.

Dr. Robert P. Magnus is the CEO and founder of Wisconsin Equine Clinic & Hospital. He runs Equine Business Management Strategies (EBMS) and founded Equine Best Practice, LLC, an equine practice financial services provider.

{kind=link}