In 2018, the future of the health insurance market became uncertain due to numerous federal changes to insurance provisions. These included the hold on cost-sharing reductions, the shortened timeframe to sign up for coverage under the federal health insurance exchange, President Trump’s executive order to allow purchase of insurance plans across state lines, and the tax package’s repeal of the individual mandate.

According to the National Conference of State Legislatures, the numbers of people who signed up for insurance during the enrollment period for 2018 through the federal and state marketplaces were just a few percentage points below the previous year. Premiums rose significantly in many counties across the country, in part due to the decision of the Trump administration to cease payments to insurers for cost-sharing reductions. Insurer participation also declined in many areas, leaving more counties with only one insurer, which likely contributed to the high rate of premium growth.

Nationally, the unsubsidized premium for the lowest-cost bronze plan increased an average of 17% between 2017 and 2018, the lowest-cost silver plan increased an average of 32%, and the lowest-cost gold plan increased an average of 18%.

With the individual mandate repealed and the ability of healthy individuals to seek low-cost insurance outside of the marketplace, premiums are destined to rise for those with pre-existing health conditions or more need for comprehensive coverage. These increases might price health insurance out of the reach of those who need it the most.

One change that could be beneficial for veterinarians is the proposed rule by the U.S. Department of Labor (DOL) that would allow small businesses to band together and purchase health insurance without some of the regulatory requirements that the individual states and the Affordable Care Act (ACA) impose on smaller employers. The proposal could make it easier for small businesses to afford better coverage for their employees.

“Many small employers struggle to offer insurance because it is currently too expensive and cumbersome,” the DOL said in a press release. “Up to 11 million Americans working for small businesses/ sole proprietors and their families lack employer-sponsored insurance … These employees—and their families—would have an additional alternative through Small Business Health Plans (Association Health Plans).”

In March 2018, a link to a 14-question survey about health insurance was distributed to equine veterinarians on the Facebook pages Equine Vet2Vet and Women in Equine Practice, as well as on the general Listserv of the AAEP. The survey was open for one week and had 247 responses. The respondents were 77% female and 23% male. Fifty-nine percent graduated in the last 15 years, but the remaining respondents were well distributed over graduation years from 2002 to before 1976.

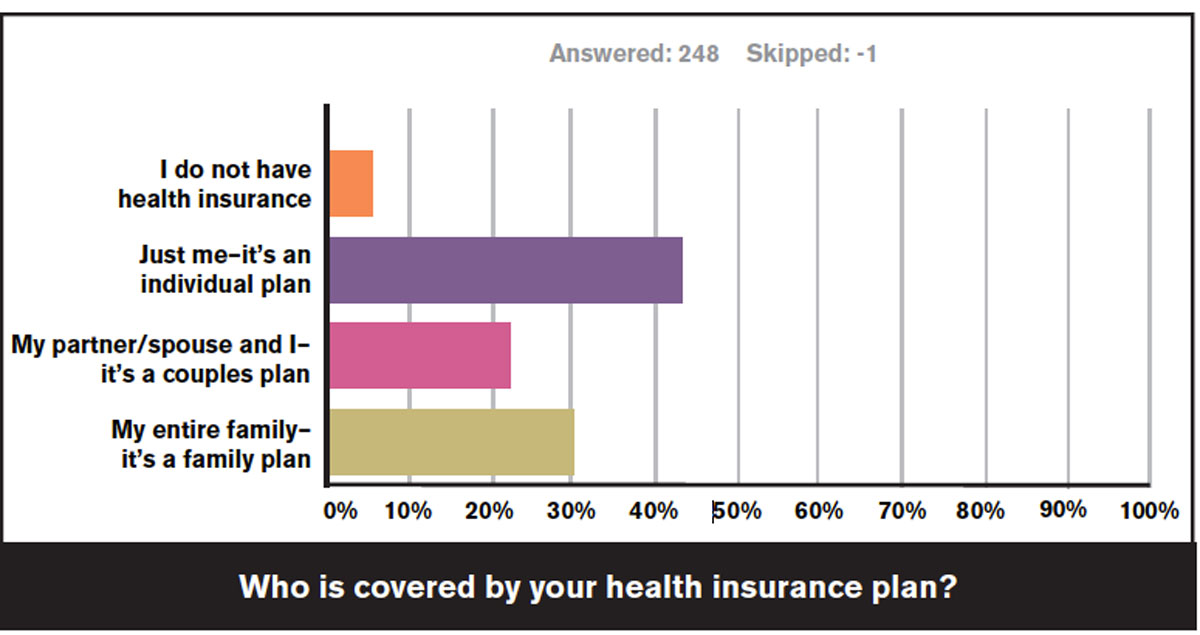

Almost all of the respondents (96.3%) reported that they have health insurance. When asked about who was covered by the plan, 43.5% indicated they have an individual plan, 22.2% have a couple’s plan and 30.6% have a family plan.

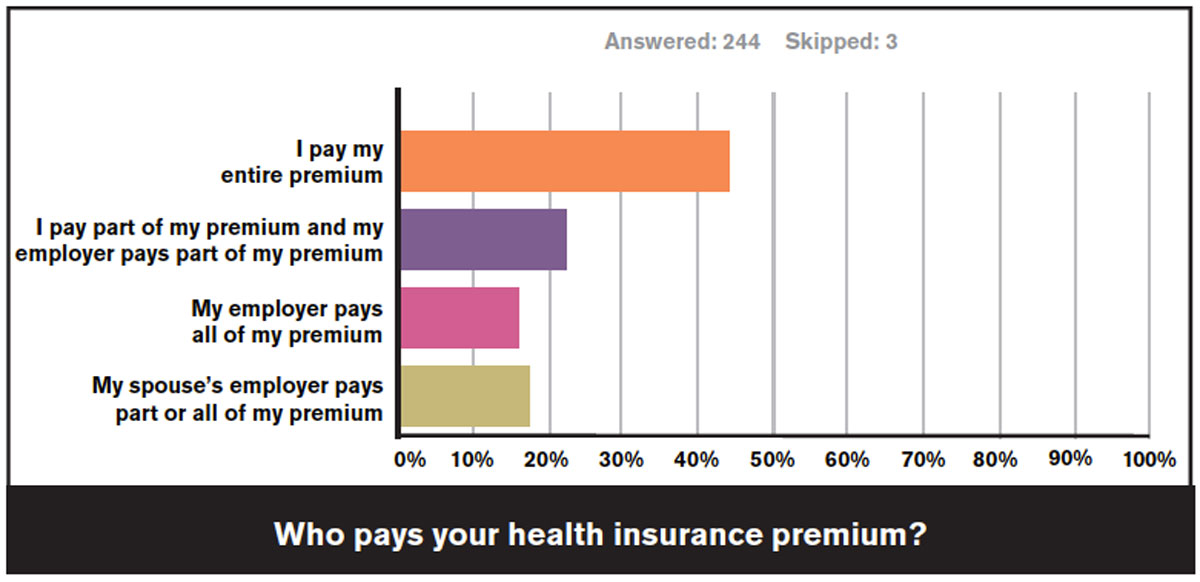

Of those with an individual plan, 50.0% reported that they pay the entire premium themselves, 30.8% said they pay part of the premium and their employers pay the remainder, and 18.7% responded that their employers pay all the cost. Fewer than 10% of these veterinarians received a subsidy for their individual coverage through the exchange.

Of the 76 respondents with a family plan, 36.8% pay the entire premium themselves, 17.1% pay part of the premium themselves and their employers pay the other part. 11.8% are fortunate to have their employers pay the entire cost, while 34.2% receive all or part of their health insurance premium through their spouses’ employers.

When all respondents are considered, 20.9% reported that their health insurance was obtained through their spouses.

Nearly 80% of respondents reported that their health insurance plan is compliant with the Affordable Care Act, 4.9% reported that it is not and 15.6% did not know. A subsidized premium was reported by only 5.7% of respondents, and 8.6% did not know whether their premium was subsidized. The majority of respondents (85.7%) did not qualify for a subsidized premium.

High-Deductible Health Plans

High-deductible health plans were reported by 39.6% of respondents. A high-deductible health plan (HDHP) is a plan with a higher deductible than a traditional insurance plan. The monthly premium is usually lower, but you pay more health care costs yourself as your deductible before the insurance company starts to pay its share.

A high-deductible plan (HDHP) can be combined with a health savings account (HSA), allowing you to pay for certain medical expenses with money free from federal taxes. The IRS defines a high-deductible health plan as any plan with a deductible of at least $1,350 for an individual or $2,700 for a family. An HDHP’s total yearly out-of-pocket expenses (including deductibles, copayments and coinsurance) can’t be more than $6,650 for an individual or $13,300 for a family. (This limit doesn’t apply to out-of-network services.)

Of those respondents who have a HDHP, 35.1% have a deductible of $6,000-$7,999, 24.7% have a deductible of $4,000-$5,999, 17.5% have a deductible of $10,000 or more, 13.4% reported $3,000-$4,999, and 3% have a deductible of $8,000-$9,999.

After meeting their deductibles, respondents with a HDHP were responsible for varying percentages of medical costs, with 22.1% having no additional contribution and 28.4% having responsibility for 11-20% of any other medical costs. Almost a third (30.5%) did not know what percentage of costs they would need to pay after their deductible was met.

A high-deductible plan can be combined with a health savings account (HSA) to allow you to pay for certain medical expenses with money free from federal taxes. Internal Revenue Code Section 223 allows individuals who are covered by a compatible HDHP health plan to set aside funds on a tax-free basis up to the contribution limit to pay for certain out-of-pocket medical expenses.

Health Savings Accounts have a triple tax benefit—funds go into the account tax-free, grow tax-free and remain completely tax-free when used for eligible medical expenses. They are owned by the participant, and can be funded by you, your employer or even a third party. HSAs carry over from year to year and are portable if employment changes.

The IRS sets the annual contribution limits and limits the types of health plans that qualify for an HSA. Contributions can be made at any time up until the tax filing deadline, typically April 15. HSA funds can be used for paying qualified medical expenses for yourself, your spouse and your dependents even if you become ineligible to contribute in the future. In 2018, the contribution limits are $3,450 for individuals and $6,900 for a family. HSA holders aged 55 and older get to save an extra $1,000, or a total of $4,450 for an individual and $7,900 for a family. These contributions are 100% tax deductible from gross income and are not taxed when spent on qualified medical expenses.

The IRS determines which expenses are eligible for reimbursement. Eligible expenses include health plan copayments, dental work and orthodontia, eyeglasses and contact lenses, and prescriptions. A comprehensive list of qualified expenses is found at: www.wageworks.com/employees/support-center/hsa-eligible-expenses-table/.

Of those survey respondents who have a HDHP, only 61.5% have an HSA account. With the significant financial benefit of these accounts, all those who qualify should consider participating.

Disability Insurance

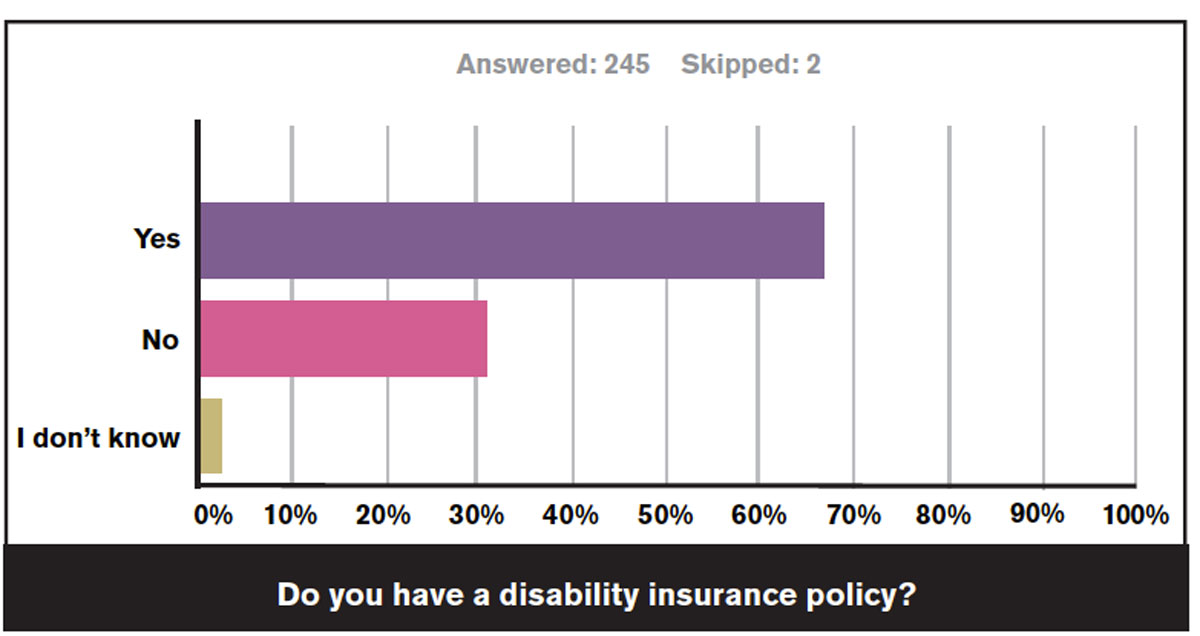

About two-thirds of respondents (66.5%) reported that they carry disability insurance. One respondent commented, “I wish I had. I am now disabled.” Another stated, “I accidentally let my AVMA disability insurance policy (which had been started at the end of vet school) expire. I then was declined by the AVMA. I have sought other policies but have found the premiums to be quite high, so I do not have a policy at this time. I’m also not sure I would pass the underwriting.”

Another wrote, “This is very important. Please promote.”

One important thing to note about disability insurance is that if you pay the premiums with after-tax dollars, the benefits you receive are tax-free. However, if your employer pays for an individual disability insurance policy for you, any benefits you receive if you are disabled will be taxable, unless you declare the premium payments each year as taxable income. Also, unlike health insurance premiums, you can’t deduct premiums paid for individual disability income insurance as a medical expense.

Long-Term Care Policies

Long-term care insurance policies help cover long-term care expenses. The phrase “long-term care” refers to the daily help that people with chronic illnesses, disabilities or other conditions need over an extended period. The type of help needed can range from assistance with simple activities (such as bathing, dressing and eating) to skilled care that’s provided by nurses, therapists or other professionals. Health insurance will not pay for daily, extended-care services.

Medicare will cover a short stay in a nursing home or a limited amount of at-home care, but only under very strict conditions.

If your income is low and you have few assets when you need care, you might quickly qualify for Medicaid. Unfortunately, to qualify for Medicaid, you must first exhaust almost all your resources and meet Medicaid’s other eligibility requirements. If you have accumulated significant assets over the course of your career, long-term care insurance can help prevent the loss of your savings and home if you should require care.

Policies offer many different coverage options. Since you can’t predict what your future long-term care needs will be, you might want to buy a policy with flexible options. Depending on the policy options you select, long-term care insurance can help you pay for the care you need, whether you are living at home or in an assisted-living facility or nursing home. The insurance might also pay expenses for adult day care, care coordination and other services. Some policies will even help pay costs associated with modifying your home, so you can keep living in it safely.

Because equine veterinary practice is physically risky, considering such a policy might be wise.

With close to 40% of the equine veterinary profession being solo practitioners, there are large numbers of folks at risk. If they are hurt on the job, there will be no Workman’s Compensation insurance to fall back on.

In this survey, 16.7% of respondents reported having a long-term care policy. 39.0% of these 41 respondents were male, and 61.0% were female. They were fairly equally distributed across graduation years, with five from 2013-2017, 10 from 2008-2012, five from 2003-2007, two from 1998-2002, seven from 1987-1997, nine from 1976-1986 and three before 1976.

Take-Home Message

While insurance for health coverage, disability and long-term care can be expensive, being prepared for unexpected events can make you and your family more secure, particularly if you have valuable—and thus vulnerable—assets.

If the unthinkable should happen, knowing that you or your family member will be able to receive care can be reassuring. It takes time to explore the available options, but it is time well spent.