Cash is the gasoline that makes your business run. Cash flow is simply the way money moves into and out of your business; it is the difference between just opening a business and having a stable year-round business. Cash-flow management is a method of checking up on your firm’s financial health to determine patterns of how you take in and pay out money.

In the slow season, incoming cash is scarce because billable revenue is lower. However, many of the daily costs to run the practice continue, or in some cases, even increase.

A cash-flow gap occurs when your cash inflows are lower than your cash outflows, leaving your business short of cash. So, how does a practice manage its cash to get all the bills paid when incoming cash is scarce and reserves may not be in the bank?

First, let’s start by defining a common financial report that your accountant sends you or your practice manager prepares called the Cash-Flow Statement. Then we can explore weekly management options that you can implement to help you maintain a positive cash flow.

We get a myriad of reports and numbers from our accountant, but without management knowledge and the ability to take corrective action, they are just numbers. Understanding the numbers and how to use them is the key to building a successful business.

Cash-Flow Statement (Report)

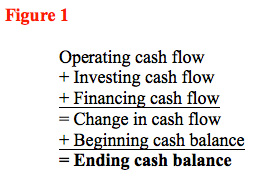

A practice’s cash flow is the movement of cash in and out of the company in the form of payments and collections. Cash flows typically arise from three sources: operations, investing and financing (Figure 1), resulting in an ending amount of cash each day, week, month, etc.

Financial institutions, such as banks and other lenders, require a Statement of Cash Flows (or Cash-Flow Statement) as one of their required financial statements for loans or lines of credit. The Statement of Cash Flows shows the movement of cash through operations (current assets and liabilities), investing (facility, equipment and investments)and financing (long- and short-term financing). Cash flows are the essential fuel to maintain a liquid and solvent business entity such as an equine practice. This report is used to help assess risk by outside lenders and also may be used as a management tool for your business to help you make better decisions. The figure below shows a monthly and year-to-date Cash-Flow Statement example.

Misconceptions

Business profits and cash flow are not the same thing. Profits are moneys that the business ends up earning after paying all expenses and taxes, while cash flow is money necessary for meeting the demands of daily operations.

The profit of the business is the bottom-line entry on the Income Statement (Profit & Loss Statement). The most common mistake made by owners is spending the cash in hand during the busy season without taking into consideration the expenses (cash outflow) that will be required during the slow season.

For example, if a practice has profits in month six of $10,000 in the busy season, it still requires operational cash (purchase meds, pay employees, etc.) in month five to get those sales. The reverse can also happen. If a company sells off equipment (assets), it may record high cash flow because of the sale revenue of the assets, but low profits because it did not sell enough services to make a profit. Companies need to keep a close eye on the cash required for “operations.” To do this, they need to look at their cash position frequently and use this type of reporting tool to manage proactively. Looking at your bank statement is not enough.

Cash-Flow Management and Forecasting

In business and in your personal life, there are really only three things we can do with cash: spend it, save it or give it away. How you manage cash will affect the company’s overall financial health.

Cash-flow management is the process of monitoring, analyzing and adjusting your company’s cash position. The most important aspect of cash-flow management is avoiding extended cash shortages caused by having too great a gap between cash inflows and outflows. You won’t be able to stay in business if you can’t pay for operations. Monitoring cash and forecasting future cash needs will help you make better management decisions and avoid or reduce the periods of the year where you don’t have enough cash to pay your bills (cost of operations).

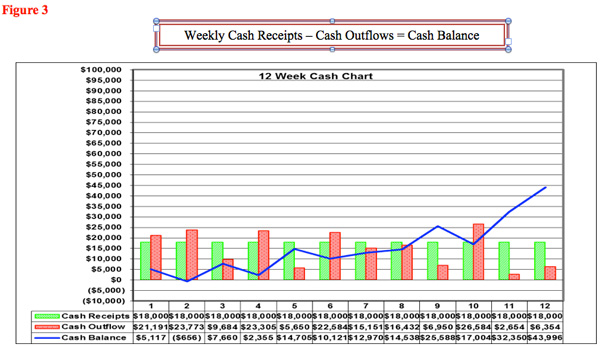

Figure 3 depicts in “week one” actual cash flow, and in the remaining 11 weeks, you see a forecast of the company’s cash position. In this depiction we are forecasting an increasing cash balance (blue line) over the 12-week period; that means more cash coming into the company than we are required to pay out. This graph is the result of input into three different spreadsheet pages that forecast revenue, accounts payable, accounts receivable and expenses based upon actual transactions and historical data, as well as known variable and fixed costs. This information is available in your practice management software and accounting software systems.

The goal of graph is to depict deficiencies or excesses in cash flow that may occur in your business during the periods for which the projection is prepared. It is a quick snapshot of where you are and where you are projected to be in the weeks to come. Your accountant, practice manager or business consultant can help you put together the details necessary to make this type of report easy to produce and meaningful to you.

This “Cash Chart” (Figure 3) is how the company owner measures the cash required for weekly operations. If you project a positive cash position, you must analyze why you are in such a fortunate state before you spend the excess cash. Some questions to consider for this owner may be:

• Is your company at the top of a business cycle (e.g., in the busy season)?

• Are you current on all of your debts?

• Have you paid your taxes, including estimated taxes?

• Do you have any “lump sum” payments due?

• While you are deciding, are those idle funds providing a reasonable rate of return (e.g., interest)?

Your objective is to develop a well-managed cash-flow plan that will allow you to predict when cash will be needed to sustain operations, as well as allow you to disburse your money prudently.

Your projections become more useful when the estimated information can be compared with actual data. Utilize your cash-flow projections to set new goals and plan operations for more profit.

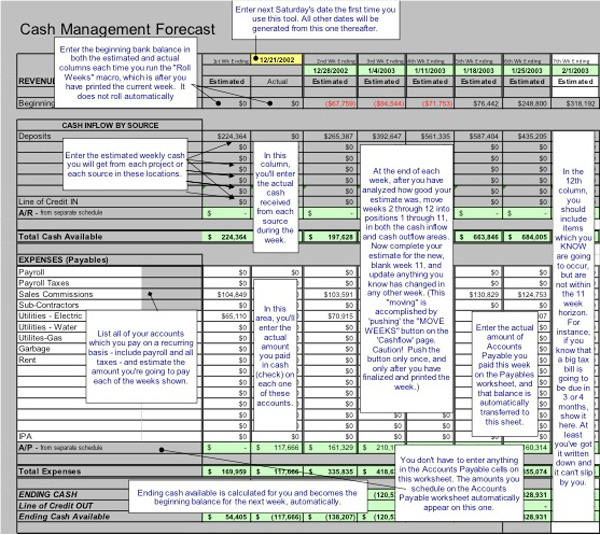

The Cash-Management Forecast Report template (above) compares actual receipts and expenditures as they become known in the columns “estimated” and “actual.” This illustrates the importance of the details necessary to drive an accurate forecasting report. This report process may be done weekly or monthly based on your resources and the level of detail you need. It looks a bit overwhelming, but is really fairly straightforward and can be customized for any size practice.

This example gives the current weekly actual that would be used in a graph such as Figure 3. Excel spreadsheets have many tools to create detailed reports that are easy to use. The remaining columns are the estimates of known and/or projected revenue and expenses.

In this example (Figure 4), the entries will require some initial background work. The captions inside Figure 4 explain the required entries. This forecast may be very simple or more detailed based on your needs.

The two other core areas, the accounts receivable and accounts payable (vendors) worksheets, are additional entries that supply the necessary actual and estimated data to complete your forecast. The weekly cash-flow report and forecast look complicated and tedious, but once set up, they are easy to update. Start slow, make it simple, then expand the value of the report. Follow through the process below to get a better understanding of where money comes in and goes out of your practice

Each column has an “Estimated” heading. Complete the forecast starting with the anticipated revenues for each week.

Anticipated revenues may be calculated by reviewing how payments on accounts receivable usually arrive. Points for consideration:

• What was the “new” billing total for last month and what percentage of the accounts receivable billed arrive during each week of a month?

• Consider confirmed payment dates on past due accounts receivable.

• Consider any new billings or cash sales that may occur during this period.

• Individual expense line items should be filled in for each week of the accounting period using historic numbers.

Include due dates of payroll, lease payments, bank loans, rent (mortgage), utilities, trash removal, etc. All these payments are entered into the appropriate week they will be due.

Normal vendor payments for medications and supplies will be listed and totaled, by week, on a separate schedule and entered as a line item called “Accounts Payable.”

Actual receipts and expenditures are to be posted at the end of each week. These receipts and expenditures must be reviewed and changes made in subsequent weeks for variances.

You now have a measure of your forecasting ability versus actual cash flow. Variances should be analyzed and adjustments made to subsequent forecasts as needed. The more you use cash- flow forecasting, the more accurate your forecasting ability will become.

Determine the company’s Cash Balance or Beginning or On-Hand Cash; enter the present cash balance (source: check book, money market, etc.) after all posting is done, or money available in the company’s bank account.

The Weekly Income is the money received at the time the product or service is delivered (not recorded as an Accounts Receivable), and deposited in the checking account.

If you have a credit line available, then you should write the total amount of the L.O.C (Line Of Credit) the bank has assigned to your account. Then enter the portion of your L.O.C. that has been used on a separate line.

Receipts on Accounts Receivable Aging: Enter the anticipated collections (source: accounts due, accounts receivable aging, average weekly deposits for the past two months, etc.) on the third page of the Cash-Flow Forecast and the total of the receipts from the Accounts Receivable will automatically be totaled and assigned to this line.

Other: This is cash anticipated from any other sources than above (such as cash from bank loans, cash sales, etc.).

Complete each week’s forecast and you will have a week-by-week forecast of planned cash requirements. Do this each accounting period. Every Cash Flow Forecast should cover a minimum of six weeks, making them overlap. There will be fluctuations from week to week, and some weeks may be negative. However, the cumulative cash flow should be positive.

Using a Weekly CashFlow Report

Once you’ve created this report, it is crucial to use it in the decision-making processes. The cash-flow position for each period should be adequate to meet the cash requirements of that period. When you project a negative cash position, cash expenditures should be reduced temporarily (possibly by delaying payments on certain line items) or cash must be injected into the business.

Whenever cash-flow deficiencies are revealed, your financial plans may need to be altered until a proper cash balance is attained. Some alternatives to consider when you project a temporary negative cash flow are:

• Increase your sales and promotions;

• Decrease your expenses;

• Defer payments to vendors as necessary and prudent;

• Obtain loans from financial institutions, including lines of credit;

• Provide cash from your personal funds;

• Monitor your customers’ use of credit and adjust their credit limits accordingly.

Consistent Cash-Flow Challenges

Consistent challenges in paying the bills or not taking a pay check due to no cash in the bank is no fun. Receiving COD shipments from the veterinary supplier is embarrassing. These are the warning signs that point to the need for changes in how you do business.

Following are a few ideas to help get cash in the door and money in the bank. They require changes by practice ownership, staff and your clients.

Invoice promptly, effectively accelerating collections. Many small businesses have a regular billing routine, such as invoicing clients and/or customers at the end of the month. This leaves money that could be sitting in the veterinarian’s bank accounts (and improving his or her cash flow) in someone else’s pockets! Instead of waiting to invoice, bill right away when the job is completed. If the clients are not present, take a credit card payment or e-invoice.

Get partial payment up front. In-stead of waiting to invoice until a job is completed, ask for a percentage of the bill to be paid before the work starts. For instance, you might charge 40% of the bill as a retainer with the remainder due on completion of the task. Or ask for a third before work starts, a third while the project is ongoing and a third upon completion. It’s a common business practice in other service industries and one you should be taking advantage of, especially if you are in financial trouble.

Give a reward for quick payment. Money you are owed, but don’t collect, is a real cash flow drain. You can get some clients to pay immediately by offering them a discount if they pay within a certain time frame, giving your cash flow a nice boost. A 2% discount for paying within 10 days is common.

Go after receivables. Regularly review your receivables and identify accounts that are overdue. Then make the phone call or send out the letter or email requesting payment. Some clients and/or customers just need reminding. When reminding doesn’t work, put the collection agency to work.

Pay bills only when they’re due. Check your suppliers’ payment terms and determine when payment is due (30, 60 or 90 days). Then wait to pay until the due dates rather than paying right away. Timing bill payments will help keep the cash in your business longer.

These are some of the quicker and more easily instituted changes you can make to get cash flow moving. Other things will probably take longer to implement, but are well worth the trouble, especially if you are having (or anticipate having) cash flow problems.

Take-Home Message

At the end of the day, the old saying “cash is king” is really true. Cash is necessary for all the daily efforts—to pay bills, invest in new growth strategies, retain a return on investment and develop healthy financial positions for the future. Understanding and implementing new ways to increase revenue, improve accounts receivable, control costs and manage the inflow and outflow of cash in a timely manner will increase cash, as well as enhance profits and the company’s value. Developing a weekly cash-flow report and forecast is a very powerful tool to consider adding to your management report dashboard. Those are numbers you can use.